Share and price trends of Private Labels by category type

NB price premia are remarkably similar across category types, but differ substantially between individual categories

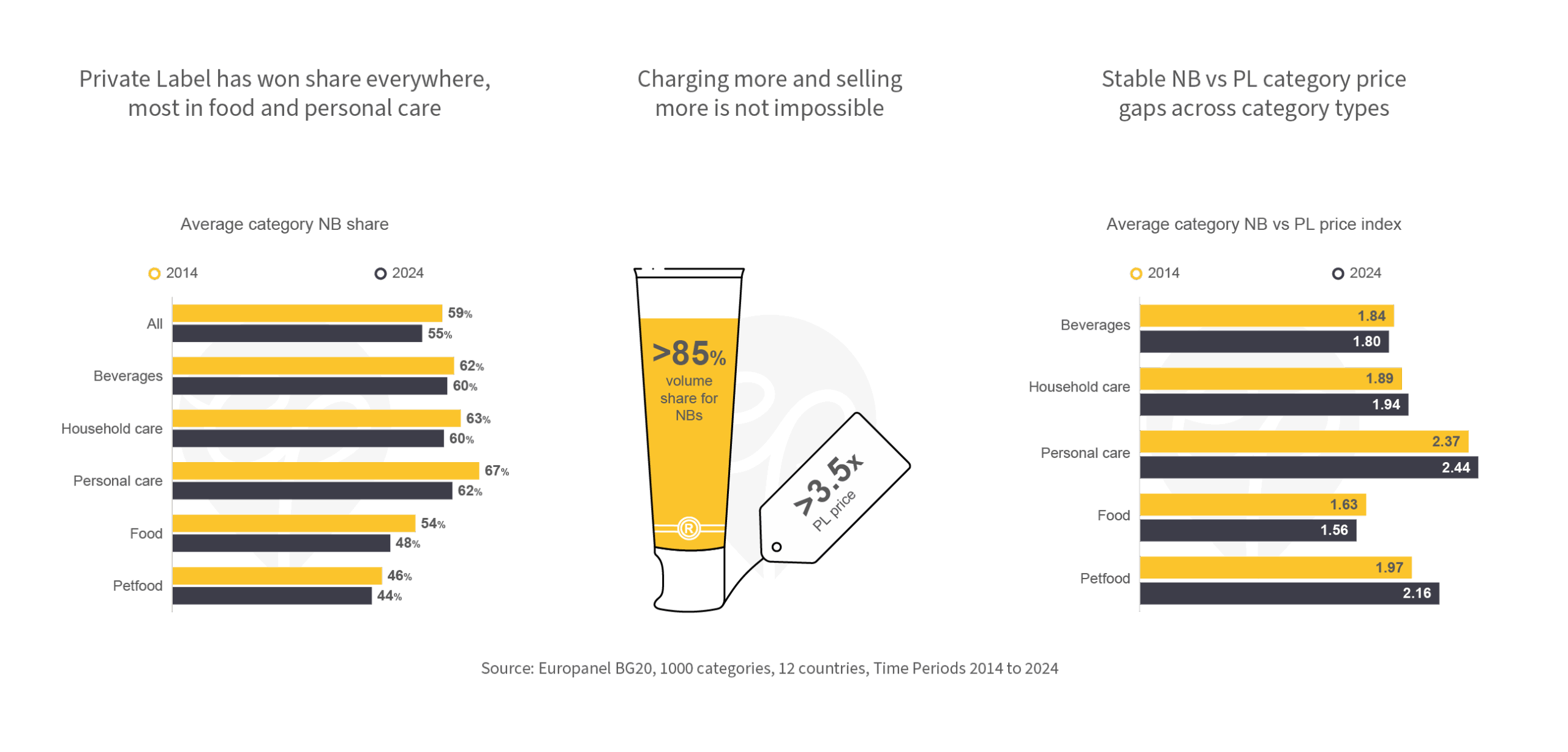

Private Label has won share everywhere, most in food and personal care

Average NB category shares have eroded by about 4% over the past decade. Beverages and household care remain relatively NB-driven, with shares slipping only marginally (from 62 % to 60 % and from 63% to 60%). Personal care is still the strongest NB stronghold, but NB share fell from 67% to 62%. The sharpest losses occurred in food, where NB share dropped from 54% to 48%. Petfood remains the most PL-penetrated segment, with NB share hovering in the mid-40s (46% to 44%).

Charging more and selling more is not impossible

We have repeatedly shown that high relative NB prices are not systematically linked to PL success. It is not unusual for categories to combine high NB premia with high NB shares – indicating that the value delivered by NBs relative to PLs justifies a much higher price. Across all twelve countries, there are several categories in which NBs on average charge at least double the PL price and hold more than 70% category share: body creams and skin care, colas, toothpaste, deodorants, fabric conditioners, hair conditioners and shampoo. In many other categories, the same pattern can be observed for specific markets.

What can you learn from these categories to maintain or enhance the equity of your own brands?

Stable NB vs PL category price gaps across category types

Average NB price premia over PL remain remarkably stable across categories. In personal care, national brands continue to command the highest relative prices, charging around 140% more than PLs in both 2014 and 2024. In food, by contrast, the average premium is much lower at about 60%. Petfood stands out as the only segment with a clear increase, with NB premia rising from roughly 100% to 120%. In summary, even though NB shares have slipped, relative prices have remained broadly stable on average.