Private Labels (PLs) on the rise during high inflation periods

As in past years of economic turbulence and high inflation, downtrading by consumers has benefitted PL.

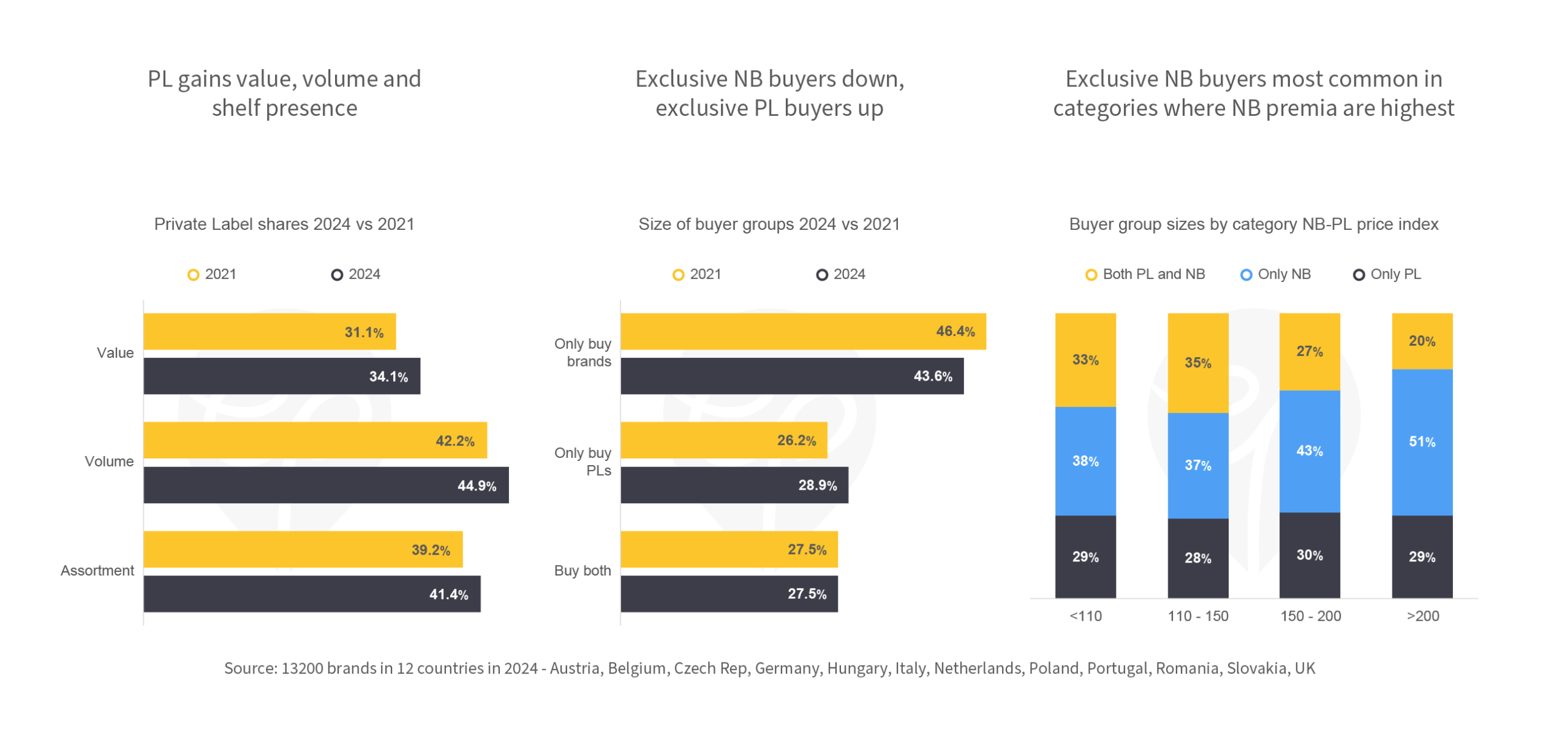

PL gains value, volume and shelf presence

Between 2021 and 2024 Europe has seen its highest inflation rates for decades (28% for the average food category in the Euro zone). One way to reduce the resulting budget crunch for households is to downgrade to less expensive choices. This tendency obviously benefits Private Labels: their share in the average category has increased by 3% in value, 2.7% in volume and 2.2% in assortment. Note that the smaller volume than value increase shows that the price increase for PLs on average has outpaced that of National Brands (NBs).

Exclusive NB buyers down, exclusive PL buyers up

In the average category, we see a drop in shoppers only choosing NB and an increase in shoppers only choosing PL between 2021 and 2024. In both years roughly one quarter of buyers pick a National Brand and a Private Label at least once. Overall this effect indicates a trickling down of some buyers from exclusive brand buying to exclusive PL buying. This aligns with past research showing that recessionary periods speed up PL gains. NBs find it difficult to win back during growth periods.

Exclusive NB buyers most common in categories where NB premia are highest

While price premia of NBs versus PLs are not consistently related to the success of NBs in a category a large price difference leads to more distinct buying of the two offerings: where NBs are more than twice as expensive as PLs half of all shoppers buy brands only, a percentage which drops to less than 40% where prices are similar. Obviously, it is not the price gap that lures these exclusive NB shoppers – but the (perceived) value gap between NB and PL that justifies higher premia that a substantial proportion of shoppers are willing to accept.

Do you track how price gaps in your category affect co-buying of private label (tiers) and specific brands?