How big are the big brands?

Somewhat smaller than in 2014, but the #1 brand on average still captures 25% of value in a category

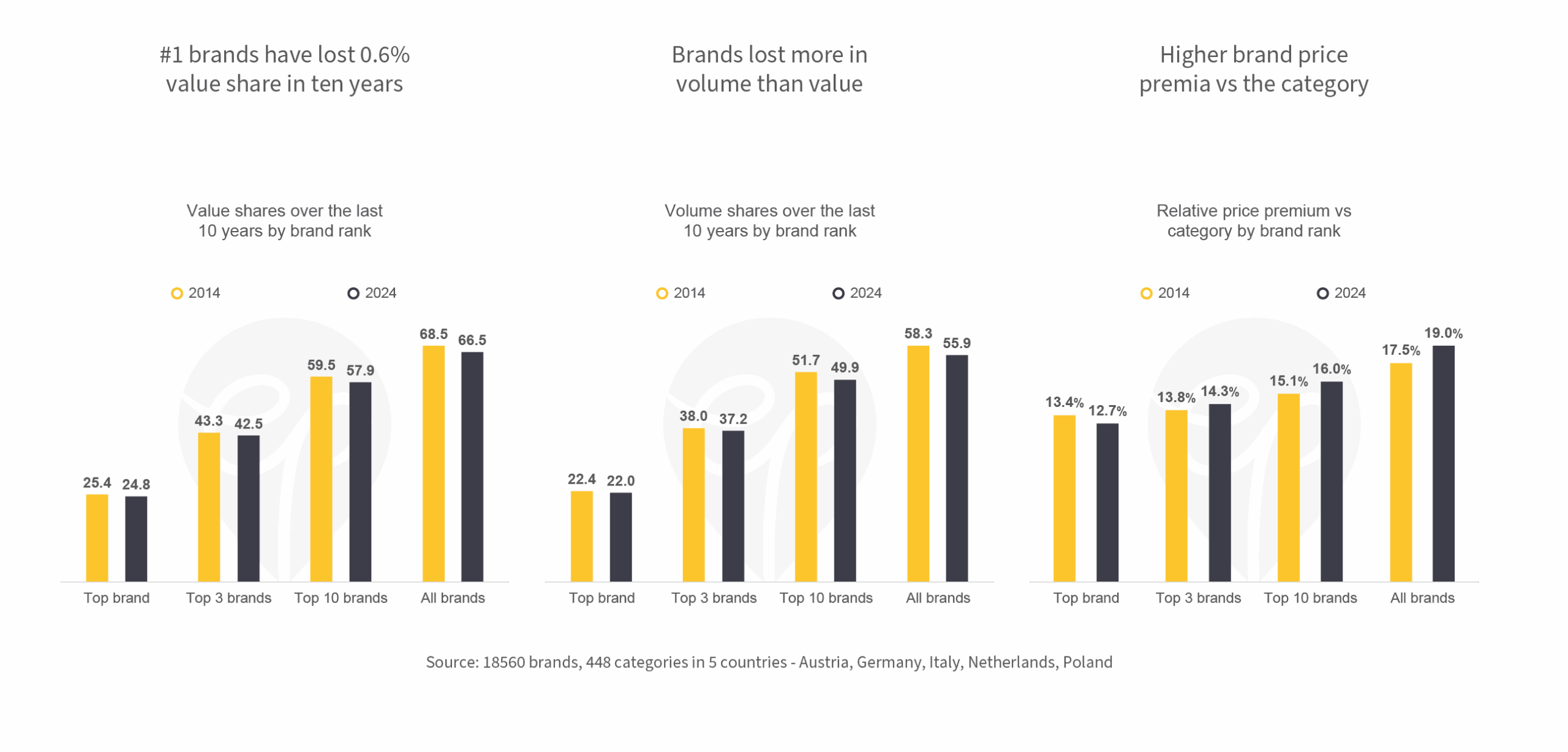

#1 brands have lost 0.6% value share in ten years

Brands of all sizes have suffered from Private Label gains over ten years (2% on average in the 448 categories covered). The top ranked brand has contributed about a third of that loss (0.6%).

Brands lost more in volume than value

Branded shares have taken a slightly bigger hit in terms of volume (minus 2.4%) than value (minus 2%) – a consequence of slightly higher prices lately. The opposite is true for #1 brands: their share decline in value exceeds their volume decline, a consequence of a smaller price premium versus the category in comparison to lower ranked brands.

Higher brand price premia vs the category

Brands have widened their price premia relative to the category, driven largely by reduced promotions during the inflation peak of 2022/2023. In addition, lower Private Label prices and rising Private Label shares will shift category price levels towards Private Label benchmarks (everything else equal).