Making sense of Private Label Success – Part 2

Its relationship with category characteristics is not always as expected

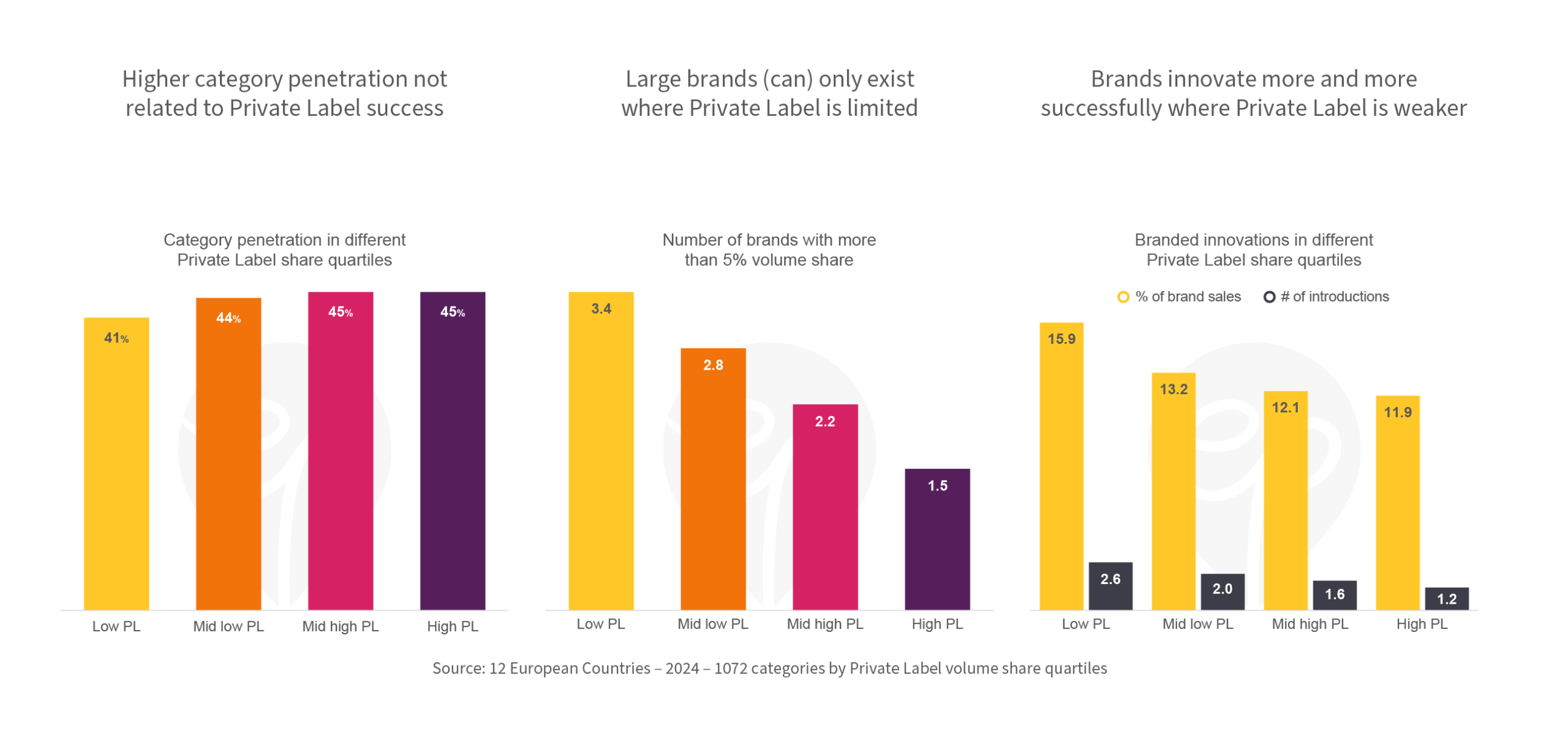

Higher category penetration not related to Private Label success

Like last week, we ranked 1072 categories by their volume Private Label shares and grouped them into four quartiles. Comparing the average category penetration in each groups shows relatively little difference. While Private Label shares are typically lower in more infrequently purchased (and hence, less penetrated) personal care categories, the average category reach is similar across all Private Label share levels.

Large brands (can) only exist where Private Label is limited

This diagram does not necessarily signal a causal link, yet strong brands, through their advertising and innovation, may help build and sustain trust in the branded offerings of a category. Once Private Label grows in importance, there simply is less space for many large brands in the room. For example in the High PL quartile national brands only have 27% of the market left. Evidence from periods of higher Private Label growth also shows how difficult it is for brands to recover share.

Brands innovate more and more successfully where Private Label is weaker

Again, the relationship depicted in the diagram is probably a two-way street. Yet, the average brand in categories with lower Private Label shares introduces more new SKUs and these launches then also capture a larger share of the brand’s total sales. Make sure you don’t lose your focus on innovation – or you may be entering a vicious cycle of eroding equity and more power to Private Labels that is hard to escape.